The nuances of filling out an advance calculation for property tax. Calculation of advance payments for property tax Filling out advance payments for property tax

Section 3 of the Calculation is completed in relation to real estate objects, the tax base for which is determined as their cadastral value. This section needs to be filled out exactly as many times as the number of “cadastral” objects the organization has. At the same time, special regime residents who have such objects are not exempt from the obligation to pay the “cadastral” tax. Since January 1, 2016, quite significant changes have occurred regarding the procedure for paying property taxes in relation to “cadastral” objects. First of all, they are related to the fact that the reporting period for the “cadastral” tax is now a quarter. Accordingly, the amount of the advance payment for the “cadastral” tax is calculated as 1/4 of the product of the tax base (cadastral value determined as of January 1, 2016) and the tax rate (Article 382 of the Tax Code). At the same time, a new procedure for calculating the “cadastral” tax has been introduced in the case where the right to an object, and, accordingly, the obligation to pay the “cadastral” tax arose (lost) in the middle of the tax period. In such cases, a special coefficient is applied when calculating the advance tax payment. It is defined as the ratio of the number of full months during which these real estate objects were owned by the taxpayer to the number of months in the tax (reporting) period. And from January 1, 2016, the month of emergence or termination of ownership in the tax (reporting) period for a “cadastral” real estate object is recognized as complete in the following cases:

- if the specified right arose before the 15th day of the corresponding month inclusive;

- when the said right is terminated after the 15th day of the relevant month.

In turn, the month of origin or termination of ownership of “cadastral” real estate is not taken into account when determining the special coefficient, if it arose after the 15th day of the corresponding month or was terminated before the 15th day of the corresponding month inclusive.

The specified special coefficient is reflected in line 080 of section. 3 Calculations. And since the reporting period for “cadastral” property is a quarter, the denominator of this fraction will always be “3”. That is, the special coefficient can take values of 1/3 or 2/3 (3/3, or 1, is not put in line 080 - if during the reporting period the ownership of the object belonged to the taxpayer for all three months of the quarter; then in this line we simply put dashes ). It is also necessary to take into account that the parties to the purchase and sale agreement for a “cadastral” object calculate the tax in relation to this real estate in a manner that depends precisely on the moment of emergence (loss) of ownership of the object. And, as the Ministry of Finance indicated in Letter dated February 2, 2016 N 03-05-04-01/4770, if the buyer-balance holder does not have the right of ownership to a real estate item included in the relevant list under Art. 378.2 of the Code, the taxpayer is the seller - the owner of the real estate property.

Which will be correct?

The company Veges LLC has been operating in the free economic zone since 04/01/2016. When submitting the report for the 1st quarter of 2016, the residual value of fixed assets as of 01/01/2016, 02/01/2016, 03/01/2016 and 04/01/2016 was taken into account. The Federal Tax Service sent a requirement to submit a corrective report for the 1st quarter of 2016. They believe that if we are in the FEZ from 04/01/2016, then for the 1st quarter we should take the residual amount of fixed assets as of 01/01/2016, 02/01/2016 and 03/01/2016.

The inspectors are wrong.

Participants of the FEZ in Crimea and Sevastopol were provided with a tax benefit on the property of organizations (clause 26 of Article 381 of the Tax Code of the Russian Federation).

Exclude preferential property from calculating the tax base, but it must still be indicated in the declaration or calculation of advance payments. First, the cost of the preferential property is included in column 3 of section 2 of the declaration (calculation), and then reflected separately in column 4 of section 2.

Thus, when filling out the calculation for the first quarter in lines 020-050 of Section 2, the organization reflects:

In column 3, the value of all fixed assets of the company that are subject to property tax, according to data as of January 1, February 1, March 1 and April 1;

In column 4 - the cost of preferential property according to data as of January 1, February 1, March 1 and April 1.

Elena Popova, State Advisor of the Tax Service of the Russian Federation, 1st rank

Attention: Since 2015, two new property tax benefits have been introduced:

– for movable property registered after December 31, 2012 (clause 25 of Article 381 of the Tax Code of the Russian Federation);

– on the property of participants in the free economic zone created in Crimea and the city of Sevastopol (clause 26 of Article 381 of the Tax Code of the Russian Federation).

Currently, there are no codes for these benefits in Appendix 6 to the Procedure for filling out the calculation of advance payments, approved. In connection with this letter dated December 12, 2014 No. BS-4-11/25774, the Federal Tax Service of Russia explained: before making appropriate changes to the order of the Federal Tax Service of Russia dated November 24, 2011 No. ММВ-7-11/895 in tax reporting property must indicate the following benefit codes:

– code 2010257 – for movable property, which is exempt from taxation in accordance with subparagraph 25 of Article 381 of the Tax Code of the Russian Federation;

– code 2010258 – for the property of participants in the free economic zone, which is exempt from taxation in accordance with subparagraph 26 of Article 381 of the Tax Code of the Russian Federation.

Fill in lines 190 and 200 if the organization has the right to a benefit established by regional legislation in the form of a reduction in the amount of the advance payment.

On line 190 in the first part of the indicator, indicate the tax benefit code 2012500, in the second part - sequentially the number, paragraph and subparagraph of the article of the regional law, in accordance with which the benefit is provided.

In line 200, enter the amount of the tax benefit, which reduces the amount of the advance payment payable to the budget.

For example, if regional authorities have established a benefit in the form of paying 80 percent of the calculated tax to the budget, then calculate the value on line 200 as follows:

| Page 200 | = | 1/4 | ? | Page 180 | ? | 100% | – | 80% | : | 100% |

Do not reflect the benefit for movable property of 3–10 depreciation groups registered after December 31, 2012 (clause 25 of Article 381 of the Tax Code of the Russian Federation) in lines 190 and 200. It should be declared on line 130. If there is no data to fill out lines 190 and 200, put a dash along the entire length of the line.

Please note: from January 1, 2015, the content of subparagraph 8 of paragraph 4 of Article 374 of the Tax Code of the Russian Federation has changed. Previously, it talked about movable fixed assets registered after December 31, 2012. Now this subparagraph refers to any fixed assets that are included in the first or second depreciation group according to the Classification approved by Decree of the Government of the Russian Federation of January 1, 2002 No. 1.

The procedure for filling out the calculation, approved by order of the Federal Tax Service of Russia dated November 24, 2011 No. ММВ-7-11/895, does not take these changes into account. Fixed assets included in the first or second depreciation group are not recognized as an object of taxation, regardless of when they were registered. However, when filling out advance payment calculations in 2017, data on their residual value must be included in the line 210 indicator. Including data on movable property (depreciation groups 1 and 2), which were registered after December 31, 2012.

An example of filling out section 2 of calculating advance payments for property tax

The Alpha organization is located in Moscow. Alpha's accountant is preparing a calculation of advance payments for property taxes for the first quarter of 2017.

Only movable property is listed on the organization's balance sheet.

According to accounting data, the residual value of movable property is:

| On the date | Residual value of movable property, rub. | Residual value of movable property registered before 01/01/2013 | Residual value of movable property registered from 01/01/2013 | ||

| Total | Total | including 1–2 depreciation groups | |||

| 1st of January | 6 765 000 | 1 014 750 | 811 800 | 5 750 250 | 4 600 200 |

| 1st of February | 6 654 791 | 998 219 | 798 575 | 5 656 572 | 4 525 258 |

| March 1 | 6 544 582 | 981 687 | 785 350 | 5 562 895 | 4 450 316 |

| April 1 | 6 878 943 | 1 031 841 | 825 473 | 5 847 102 | 4 677 681 |

Movable property included in the first and second depreciation groups are not recognized as an object of taxation, regardless of when they were registered. However, when filling out advance payment calculations in 2017, the accountant included data on their residual value in the line 210 indicator.

The accountant declared the benefit for movable property (3–10 depreciation group) registered after December 31, 2012 (clause 25 of Article 381 of the Tax Code of the Russian Federation) on line 130.

The accountant filled out Section 2 of the calculation as follows.

In column 3, lines 020–050, the accountant indicated the residual value of property recognized as an object of taxation (including preferential) as of:

- January 1 – RUB 1,353,000. (RUB 6,765,000 – RUB 811,800 – RUB 4,600,200);

- February 1 – RUB 1,330,958. (RUB 6,654,791 – RUB 798,575 – RUB 4,525,258);

- March 1 – RUB 1,308,916. (RUB 6,544,582 – RUB 785,350 – RUB 4,450,316);

- April 1 – RUB 1,375,789. (RUB 6,878,943 – RUB 825,473 – RUB 4,677,681).

- January 1 – 1,150,050 rub. (RUB 5,750,250 – RUB 4,600,200);

- February 1 – RUB 1,131,314. (RUB 5,656,572 – RUB 4,525,258);

- March 1 – RUB 1,112,579. (RUB 5,562,895 – RUB 4,450,316);

- April 1 – RUB 1,169,420. (RUB 5,847,102 – RUB 4,677,681).

On line 120 - the average cost of all property for the first quarter:

(RUB 1,353,000 + RUB 1,330,958 + RUB 1,308,916 + RUB 1,375,789): 4 = RUB 1,342,166

On line 130 - tax benefit code 2010257 according to the letter of the Federal Tax Service of Russia dated December 12, 2014 No. BS-4-11/25774.

On line 140 – the average cost of preferential property for the first quarter:

(RUB 1,150,050 + RUB 1,131,314 + RUB 1,112,579 + RUB 1,169,420): 4 = RUB 1,140,841

On line 170 - the property tax rate for organizations in Moscow is 2.2 percent (Moscow Law of November 5, 2003 No. 64).

On line 180 - the amount of the advance payment for property tax for the first quarter, calculated using the formula:

(RUB 1,342,166 – RUB 1,140,841) ? 2.2%: 4 = 1107 rub.

On line 210 - the residual value of all fixed assets as of April 1: RUB 6,878,943.

Vladislav Volkov answers:

Deputy Head of the Department of Taxation of Personal Income and Administration of Insurance Contributions of the Federal Tax Service of Russia

“Inspectors will compare the income of individuals in 6-NDFL with the amount of payments calculated for insurance premiums. Inspectors will begin to apply this control ratio starting with reporting for the first quarter. All control ratios for checking 6-NDFL are given in. For instructions and samples of filling out 6-NDFL for the first quarter, see the recommendations.”

The procedure for filling out and submitting calculations for advance payment of property tax for 9 months of 2016

Let's consider the procedure for filling out and submitting an advance payment for property tax for 9 months of 2016.

When is the advance payment for property tax due?

Companies that have movable and immovable property are obliged no later than 30 calendar days from the end of the quarter to submit to the inspectorate a tax calculation for the advance payment of property tax (clause 2 of Article 386 of the Tax Code of the Russian Federation).

The deadline for submitting calculations for the advance payment of property tax for 9 months of 2016 is until October 30. But since this day falls on a Sunday, the deadline for submitting the calculation is postponed to October 31.

The calculation form and the procedure for filling it out were approved by order No. ММВ-7-11/895 dated November 24, 2011.

Reporting periods

Reporting periods may vary. Reporting periods depend on how the organization calculates taxes. If based on the average value of property, then the periods will be the first quarter, six months and nine months. It turns out that the deadline for submitting a property tax return for 9 months of 2016 expires based on the results of 9 months of 2016.

For companies that calculate tax from the cadastral value of property, the periods are considered to be the first quarter, second quarter and third quarter (clause 2 of Article 379 of the Tax Code of the Russian Federation). At the same time, the code allows regions not to establish reporting periods (clause 3 of Article 379 of the Tax Code of the Russian Federation). Therefore, if the company is located in a region that has taken advantage of this norm and does not have periods, then it only needs to submit a declaration for the year.

If the residual value of the fixed asset is zero

The company must submit calculations of advance payments for property tax even if the residual value of fixed assets is zero.

The Tax Code does not make any exceptions for such cases.

It’s just that for fully depreciated objects, the tax base and the amount of tax that must be indicated in the calculations will be equal to zero. However, the organization is obliged to submit a calculation if at least one fixed asset is listed on its account 01 (letter of the Federal Tax Service of Russia dated 02/08/10 No. 3-3-05/128).

But the deadline for submitting calculations for the advance payment of property tax for 9 months of 2016 for a zero report is the same as for a regular one - until October 31, 2016.

Zero calculation for advance payment of property tax in the absence of taxable property

If an organization does not have taxable property, then it is not recognized as a property tax payer and does not have to submit a declaration (Letter of the Ministry of Finance dated February 28, 2013 N 03-02-08/5904.

Thus, there is no need to submit a calculation if the balance sheet reflects only property that is not recognized as an object of taxation on the basis of subparagraphs 1-7 of paragraph 4 of Article 374 of the Tax Code of the Russian Federation

For example, if a company has only land plots and has no other property.

Where to submit the calculation for the advance payment of property tax for 9 months of 2016

Companies must submit calculations for advance payments of property tax to the inspectorate:

At your place of registration. This also applies to real estate located at the place of registration of the company;

At the location of each separate division. If the division has its own balance sheet and the property is listed on it;

At the location of the real estate, if it is located separately from the parent organization and separate divisions.

In what form should I submit an advance payment for property tax?

The company has the right to send the calculation of the advance payment for property tax to the inspectorate in different ways:

On paper directly to the inspectorate. Then the calculation is drawn up in two copies in order to put a mark of acceptance on one. You can hand over in person or through a power of attorney. Sometimes the inspection may ask the company to attach a calculation file in electronic form on a floppy disk or flash drive;

On paper by mail. It is sent by a valuable letter with an inventory of the contents;

In electronic form via telecommunication channels.

Companies whose average number of employees exceeds 100 people are required to submit calculations electronically (clause 3 of Article 80 of the Tax Code of the Russian Federation).

Regardless of the method of submission and the number of employees, the deadline for submitting the property tax return for the 3rd quarter of 2016 does not change.

Responsibility for failed payment

For violating the deadline for submitting an advance payment for property tax for 9 months of 2016 or failing to submit it, the company will be fined 200 rubles for failure to submit a document (Clause 1 of Article 126 of the Tax Code of the Russian Federation).

Moreover, it does not matter that the tax can be paid before the calculation is submitted.

In addition, a fine in the amount of 300 to 500 rubles may be imposed (Part 1 of Article 15.6 of the Code of Administrative Offenses of the Russian Federation).

But under Article 119 of the Tax Code of the Russian Federation, the company will not be fined, since the calculation of advance payments is not a tax return (clause 1 of Article 80 of the Tax Code of the Russian Federation).

Property tax rates

The maximum property tax rates are determined in the Tax Code.

For 2016, the following maximum rates are established:

1) 2.2 percent– for all property not specified below;

2) 2 percent– for real estate on which the tax is calculated based on the cadastral value in Moscow (in fact, in 2016 in Moscow there is a rate of 1.3%, and for some real estate this rate is applied with a coefficient of 0.1. This is stated in Articles 2 and 3 Law of Moscow dated November 5, 2003 No. 64);

3) 2 percent– for real estate, on which the tax is calculated based on the cadastral value for all constituent entities of the Russian Federation, except Moscow;

4) 1.3 percent– along public railway tracks, main pipelines, energy transmission lines, as well as structures that are an integral part of the listed facilities;

5) 0 percent– for real estate objects of main gas pipelines and structures that are their integral technological part, gas production, helium production and storage facilities, for which the following conditions are simultaneously met:

objects are located wholly or partially within the borders of the Republic of Sakha (Yakutia), Irkutsk or Amur region;

the objects belong by right of ownership to organizations that are the owners of the objects of the Unified Gas Supply System or organizations in which the owners of the objects of the Unified Gas Supply System participate.

Regional authorities, taking into account these restrictions, determine the tax rates at which property taxes must be calculated and paid in a particular subject of the Russian Federation. Moreover, in the regions they can set several different rates for different categories of organizations and property. In any case, regional rates cannot exceed the maximum values established at the federal level. What rates should be applied if the authorities of a constituent entity of the Russian Federation have not determined them? In this case, calculate the tax at the maximum rates.

Organizations that have separate divisions with separate balance sheets or geographically distant real estate in different regions must apply the rates established in the corresponding regions when calculating property tax.

All this follows from paragraphs 1 and 2 of Article 372, Articles 380, 384 and 385 of the Tax Code of the Russian Federation.

Calculation sections for advance payment of property tax

Advance payment includes:

Title page;

Sec. 1, intended to reflect the amount of tax payable to the budget;

Sec. 2 , intended for calculating tax based on book value;

Sec. 3 , intended for calculating tax based on cadastral value.

You must submit all advance payment sheets to the Federal Tax Service, even if you do not have objects that should be reflected in section. 2 or 3.

The procedure for filling out the calculation for the advance payment of property tax

First you need to fill out a cover page, in which you should indicate information about the organization and the declaration being submitted.

Then section is filled in. 3, section 2 and at the end - section. 1.

Section 3 of calculation of advance payment for property tax

Section 3 of the declaration is filled out for each property, the tax on which is calculated based on the cadastral value (Letter of the Federal Tax Service dated October 16, 2014 N BS-4-11/21488).

Accordingly, you need to fill out so many sections. 3, how many such real estate objects does the Organization have?

If the Organization does not have real estate taxed based on cadastral value, then in Sec. 3 dashes are added in all fields except TIN, KPP, Page. (Clause 2.4 of the Procedure for filling out the declaration).

If the property did not belong to the organization during the entire reporting period, then in line 080 indicate the coefficient, defined as the ratio of the number of full months during which the property was owned to three (the number of months in the reporting period). In this case, a full month is taken in which (clause 5 of Article 382 of the Tax Code of the Russian Federation):

The ownership of the object is registered if this happened before the 15th day of the month inclusive. If ownership of an object is registered after the 15th day, then this month is not taken into account when calculating the tax;

The termination of ownership of the object is registered if this occurred after the 15th day of the month. If the termination of ownership of an object is registered before the 15th day inclusive, then this month is not taken into account when calculating the tax.

Line 080 is given as a proper fraction. It can be 1/3 or 2/3.

If the company owned the property for the entire quarter, there is no need to fill out line 080 with a ratio of 3/3.

After all, the amount of the advance payment in this case is not subject to adjustment. In this case, dashes are placed in line 080.

For example, if ownership of a property was registered on August 15, 2016, then you owned the property for eight months in Q3.

In line 080 section. 3 calculations for the 3rd quarter, make an entry 2/3 (clause 5 of Article 382 of the Tax Code of the Russian Federation, clause 7, clause 6.2 of the Procedure for filling out the calculation for an advance payment).

Section 2 of calculation of advance payment for property tax

For example, if an Organization has two buildings with different OKTMO codes on the territory controlled by one Federal Tax Service Inspectorate, you need to fill out two sections. 2.

If, in addition, a reduced tax rate is established for part of the property, then another section should be completed. 2.

In line 270 section. 2 indicates the residual value of all fixed assets of the organization, except land plots, including:

fixed assets included in the first or second depreciation group (Letter of the Federal Tax Service dated 08/07/2015 N BS-4-11/13906@);

Objects taxed based on cadastral value;

Property listed on the balance sheet of the OP.

Moreover, if the Organization reports at the location of both the organization and the OP, then in both declarations the indicator is line 270, section. 2 will be the same (Letter of the Federal Tax Service dated 05/08/2014 N BS-4-11/8871).

Section 1 of calculation of advance payment for property tax

In Sect. 1 of the calculation to reflect the amount of the advance payment payable according to the corresponding OKTMO code, seven blocks of lines 010 - 030 are provided, which indicate:

In line 010 - OKTMO code, according to which the amount of the advance payment is due;

On line 020 - KBK 182 1 06 02010 02 1000 110;

On line 030 - amount to be paid.

If you calculate property tax using one OKTMO code, based on both book value and cadastral value, then in line 030 section. 1 Enter the total amount to be paid. It consists of two amounts (clause 4.2 of the Procedure for filling out the calculation for an advance payment, Letter of the Federal Tax Service dated 05/08/2014 N BS-4-11/8876):

The amount of the advance payment calculated on the basis of the book value of property with the same OKTMO code;

The amount of the advance payment calculated on the basis of the cadastral value of property with the same OKTMO code.

Reflection of the accrual and payment of property tax in accounting and tax accounting

In accounting property tax, calculated both on the basis of the book value and on the basis of the cadastral value, and advance payments on it are accrued by transactions:

When transferring property taxes, the posting will be as follows:

For purposes income tax property tax and advance payments on it are taken into account as expenses on the accrual date, regardless of the date of payment to the budget (clause 1, clause 1, article 264, clause 1, clause 7, article 272 of the Tax Code of the Russian Federation, Letter of the Ministry of Finance dated 09.21.2015 N 03-03-06/53920).

In the declaration for property tax and advance payments thereon, they are reflected on line 041 of Appendix No. 2 to Sheet 02 on an accrual basis in the total amount of taxes and fees accrued in the reporting (tax) period (clause 7.1 of the Procedure for filling out the declaration).

Calculation of the tax base and tax based on the “cadastral” value

To calculate the tax base for cadastral property, the company must know its value.

Information on the cadastral value can be taken from the state real estate cadastre (Article 7 of the Federal Law of July 24, 2007 No. 221-FZ).

A company can find out the value of a specific asset on the Rosreestr website.

When calculating tax based on the “cadastral” value of property, the company can use the calculation formula (clauses 1, 2 and 4 of Article 382 of the Tax Code of the Russian Federation):

Advance tax payment = Cadastral value of property as of January 1 of the tax period x tax rate / 4

If the cadastral value of the premises owned by the organization has not been determined, but the cadastral value of the building in which it is located has been determined, the value of this premises is determined by the formula (clause 6 of Article 378.2 of the Tax Code of the Russian Federation):

Tax base for premises, the cadastral value of which has not been determined = Cadastral value of the building (as of January 1 of the current year) in which the premises are located/Total area of the building X Area of the premises

It is important when the organization became the owner. It is he who pays the property tax on the cadastral value (subclause 3, clause 12, article 378.2 of the Tax Code of the Russian Federation).

Before registering the transfer of ownership, the previous owner of the property must pay tax at the cadastral value.

And the new owner, when calculating the tax in 2016, must take into account the so-called ownership coefficient (clause 5 of Article 382 of the Tax Code of the Russian Federation).

If ownership of a real estate item arose or ceased during the reporting period (I, II or III quarter), then the amount of the advance payment payable on such an object for the reporting period is calculated taking into account the number of full months during which you owned it in reporting period.

In this case, a full month is taken in which (clause 5 of Article 382 of the Tax Code of the Russian Federation):

The ownership of the object is registered if this happened before the 15th day of the corresponding month inclusive. If ownership of an object is registered after the 15th day, then this month is not taken into account when calculating the advance tax payment;

The termination of ownership of the object is registered if this occurred after the 15th day of the corresponding month. If the termination of ownership of an object is registered before the 15th day inclusive, then this month is not taken into account when calculating the advance tax payment.

Then the amount of the advance payment for an incomplete reporting period is calculated using the formula:

Advance tax payment = (Cadastral value of property as of January 1 of the tax period x tax rate) / 4 x (Number of full months of property ownership in the reporting period / 3)

Calculation of the tax base and tax based on the average annual value of property

The tax base for the remaining property is calculated based on its average annual value (clause 4 of Article 376 of the Tax Code of the Russian Federation).

First, the residual value of the property is calculated:

Residual value = original cost – accrued depreciation;

The residual value is determined according to accounting data and is equal to the original cost of fixed assets (debit balance of accounts 01 “Fixed Assets”, 03 “Income Investments in Material Assets”) minus accrued depreciation (credit balance of account 02 “Depreciation of Fixed Assets”) (clause 3 of Art. 375 Tax Code of the Russian Federation).

Average value of the Property = (residual value at the beginning of the tax period + remaining value at the beginning of each month + remaining value at the beginning of the first month after the reporting month) / (number of months in the reporting period (3,6, or 9) + 1);

Advance tax payment = average property value x tax rate / 4

Example. Calculation of the average and average annual value of property, advance payments and property tax for 2016

Residual value of OS:

As of 01/01/2016 - RUB 1,500,000;

As of 02/01/2016 - RUB 1,450,000;

As of 03/01/2016 - RUB 1,400,000;

As of 04/01/2016 - RUB 1,350,000;

As of 05/01/2016 - RUB 1,300,000;

As of 06/01/2016 - RUB 1,250,000;

As of 07/01/2016 - RUB 1,200,000;

As of 08/01/2016 - RUB 1,150,000;

As of September 1, 2016 - RUB 1,100,000;

As of 10/01/2016 - RUB 1,050,000;

As of November 1, 2016 - RUB 1,000,000;

As of December 1, 2016 - RUB 950,000;

As of December 31, 2017 - RUB 900,000.

The property tax rate in a constituent entity of the Russian Federation is 2.2%.

1. Calculation of the advance payment for the first quarter.

The average cost of property is RUB 1,425,000. ((RUB 1,500,000 + RUB 1,450,000 + RUB 1,400,000 + RUB 1,350,000) / 4).

Advance payment for the first quarter - 7838 rubles. (RUB 1,425,000 x 2.2% / 4).

2. Calculation of advance payment for six months.

The average cost of property is RUB 1,350,000. ((RUB 1,500,000 + RUB 1,450,000 + RUB 1,400,000 + RUB 1,350,000 + RUB 1,300,000 + RUB 1,250,000 + RUB 1,200,000) / 7).

Advance payment for half a year - 7425 rubles. (RUB 1,350,000 x 2.2% / 4).

3. Calculation of advance payment for 9 months.

The average cost of property is RUB 1,275,000. ((RUB 1,500,000 + RUB 1,450,000 + RUB 1,400,000 + RUB 1,350,000 + RUB 1,300,000 + RUB 1,250,000 + RUB 1,200,000 + RUB 1,150,000 + RUB 1,100,000 + RUB 1,050,000) / 10).

Advance payment for 9 months - 7013 rubles. (RUB 1,275,000 x 2.2% / 4).

4. Calculation of property tax for the year.

The average annual value of property is RUB 1,200,000. ((RUB 1,500,000 + RUB 1,450,000 + RUB 1,400,000 + RUB 1,350,000 + RUB 1,300,000 + RUB 1,250,000 + RUB 1,200,000 + RUB 1,150,000 + RUB 1,100,000 + RUB 1,050,000 + RUB 1,000,000 + RUB 950,000 + RUB 900,000) / 13).

Property tax for the year - 26,400 rubles. (RUB 1,200,000 x 2.2%).

The tax payable for the year is RUB 4,124. (RUB 26,400 - RUB 7,838 - RUB 7,425 - RUB 7,013).

Then section 2 should be completed as follows:

Section 2

This section reflects the residual value of fixed assets as of the first day of each month of the year on lines 020 - 110

For each of these lines, column 3 shows the residual value of fixed assets recognized as an object of taxation, and column 4 shows the value of preferential property. Since the company does not have benefits, column 4 will remain empty.

The average value of property for the reporting period is shown on line 120.

Lines 130, 140 and 150 are provided to reflect the tax benefit code, the average annual value of tax-free property and the share of the book value of the property in the territory of the corresponding constituent entity of the Russian Federation. Since the organization in our example does not have preferential property and all the real estate it owns is located on the territory of one constituent entity of the Russian Federation, lines 130, 140, 150 remain empty.

Line 160 is provided for the tax benefit code established in the form of a reduced tax rate. In our case, it will remain empty, since the company does not use preferential rates.

Line 170 indicates the tax rate - 2.2%.

The amount of the advance payment for the reporting period is reflected in line 180.

Lines 190, 200 show the code and amount of the tax benefit, which reduces the amount of tax payable to the budget.

Since the organization does not have benefits, these lines will remain empty.

Line 210 reflects the residual value of fixed assets as of 01.10 of the reporting period.

Example. Calculation of property tax on a property accepted on the balance sheet on December 31, 2015.

In December 2015, the organization acquired a building to house offices in Moscow. The object was accepted on the balance sheet on December 31. According to accounting data, the residual value of the building as of this date is 17,000,000 rubles. The tax rate is 2.2 percent.

From January 1, 2016, the cadastral value of 40,000,000 rubles was established for this object. The tax rate is 1.3 percent.

Since 2016, the tax base for this property is the cadastral value.

2015

The average property value is:

17,000,000 rub.: (12 + 1) = 1,307,692 rub.

Tax amount for 2015:

RUB 1,307,692 × 2.2% = RUB 28,769

2016

The organization owns the property for 10 months (March–December). The value of the adjustment coefficient for calculating property tax (advance payments) is equal to:

1/3 – for the first quarter;

3/3 – for the second quarter;

3/3 – for the third quarter;

10/12 – per year.

The amount of advance payments is equal to:

40,000,000 rub. × 1.3% × 1/3: 4 = 43,333 rub. – for the first quarter of 2016;

40,000,000 rub. × 1.3% × 3/3: 4 = 130,000 rub. – for the second quarter of 2016;

40,000,000 rub. × 1.3% × 3/3: 4 = 130,000 rub. – for the third quarter of 2016.

The amount of property tax to be paid additionally at the end of 2016 will be:

40,000,000 rub. × 1.3% × 10/12 – (43,333 rub. + 130,000 rub. + 130,000 rub.) = 130,000 rub.

Then section 3 should be completed as follows:

Section 3

This section is completed for real estate objects, the tax base for which is the cadastral value.

Please note that the section shows the tax calculation for one property. This follows from the provisions of paragraphs. 1 and 2 clause 6.2 Procedure for filling out the declaration. That is, section 3 declarations will be as many as the organization has real estate objects for which the tax is calculated based on the cadastral value.

In the example we are considering, the organization has only one such object. Therefore, Sec. There will also be only one 3 declarations.

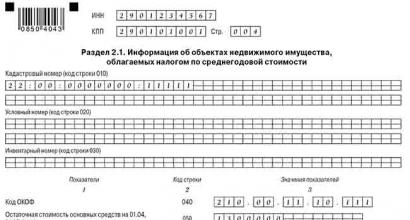

In line 014, the organization will reflect the cadastral number of the property, and in line 020 its cadastral value as of January 1, 2016.

Line 030 is provided to reflect the tax-free cadastral value. In our case, it will remain empty, since the entire cadastral value of the property is taxed.

Lines 040 and 070 contain tax benefit codes. Since the organization does not have benefits, these lines will be empty.

Line 050 is filled in when the property has an actual location on the territories of different constituent entities of the Russian Federation or on the territory of a constituent entity of the Russian Federation and in the territorial sea of the Russian Federation (on the continental shelf of the Russian Federation or in the exclusive economic zone of the Russian Federation) (clause 4, clause 6.2 of the Procedure for filling out the declaration). Since all of the organization’s real estate is located on the territory of one constituent entity of the Russian Federation, this line remains empty.

Line 070 shows the tax base. It represents the difference between the values of lines 020 and 030 (clause 5, clause 6.2 of the Procedure for filling out the declaration).

Since line 030 is empty, the value on line 060 will be equal to the value on line 020, that is, 40,000,000 rubles.

Line 070 indicates the tax rate. In our case it is 1.3%.

Line 080 indicates the coefficient K. In our case it is 1.

The amount of the advance payment for the reporting period is reflected on line 090.

Lines 100 and 110 will remain blank, since the organization does not have benefits.

As of reporting for 2017, the following were approved: new tax return forms and calculations for advance payment of corporate property tax, the procedure for filling them out and electronic format (Order of the Federal Tax Service No. ММВ-7-21/271@ dated 03/31/2017).

The previous tax return and tax calculation forms, as well as the procedure for filling them out and electronic formats, approved by Order of the Federal Tax Service of Russia dated November 24, 2011 No. ММВ-7-11/895, will become invalid as of June 13, 2017.

The new declaration form is mandatory starting with reporting for the tax period of 2017. It can also be used during the liquidation (reorganization) of an organization in 2017 until June 13, 2017 (letter of the Federal Tax Service of Russia dated April 14, 2017 No. BS-4-21/7139@).

And the new form of tax calculation for advance payment is allowed for use at the initiative of the taxpayer, starting with calculations for the first quarter of 2017 - if it is necessary to fill out the calculation taking into account the changes in corporate property tax that have entered into force.

Who submits the reports

Organizations that have property recognized as an object of taxation (clause 1 of Article 373 of the Tax Code of the Russian Federation) must report using new forms. For Russian organizations, taxable property includes (clause 1 of Article 374, clauses 1, 7 of Article 378.2 of the Tax Code of the Russian Federation):

- movable property and real estate reflected in accounting (including leased, temporary possession, trust management, contributed to joint activities or received under a concession agreement);

- real estate from the list of objects approved in the subject of the Russian Federation, taxed at cadastral value, namely: administrative and business centers and shopping centers (complexes) and premises in them, offices, retail facilities, public catering and consumer services, as well as residential buildings and premises not reflected in accounting as fixed assets.

At the same time, the objects listed in paragraph 4 of Article 374 of the Tax Code of the Russian Federation are not subject to property tax for organizations, including:

- land plots and other environmental management facilities;

- objects recognized as objects of cultural heritage (historical and cultural monuments) of the peoples of the Russian Federation of federal significance;

- ships registered in the Russian International Register of Ships;

- fixed assets included in the first or second, etc.

What has changed in the calculation of advance payments?

The barcodes on all calculation pages have changed, and the field for indicating the Taxpayer Identification Number has been reduced from 12 to 10 characters. Fundamental innovations affected the title page, sections 2 and 3. In addition, a new section 2.1 “Information on real estate objects taxed at the average annual value” appeared.

Cover page of calculation

Firstly, it is no longer necessary to indicate according to the All-Russian Classifier of Types of Economic Activities.

Secondly, the reporting period codes have changed (see Table 1).

Table 1

Changing reporting period codes in advance payment calculations

Section 2 calculations

Unlike the previous calculation form, section 2 should be filled out separately and also according to:

- main gas pipelines, gas production facilities, helium production and storage facilities;

- other objects necessary to ensure the functioning of real estate objects of main gas pipelines, gas production facilities, helium production and storage facilities.

- objects are located wholly or partially within the borders of the Republic of Sakha (Yakutia), Irkutsk or Amur region;

In addition, the property type codes required to fill out line 001 of section 2 of the calculation have changed and become two-digit. In particular, separate codes are now installed:

- 11 – for real estate objects included in the list of objects for which the tax base is determined

New tax benefit codes have been added that are required to fill out line 130 of section 2 of the calculation, namely:

- 2010257 - for movable property registered as fixed assets from 01/01/2013 (with the exception of railway rolling stock produced starting from 01/01/2013), registered as a result of the reorganization or liquidation of legal entities or the transfer, including acquisition, of property between interdependent persons;

- 2010258 - in relation to property recorded on the balance sheet of an organization - a participant in a free economic zone (FEZ), created or acquired for the purpose of conducting activities in the territory of a FEZ and located on the territory of this FEZ, for 10 years from the month following the month of registration of the specified property.

A new line 175 has appeared to indicate the Kzd coefficient.

It is filled in if code 09 is indicated on line 001 of section 2 of the calculation - in relation to public railway tracks and structures that are their integral technological part, first registered as fixed assets, starting from 01/01/2017.

Section 2.1 calculation

This section will have to be filled out by Russian and foreign organizations in relation to the real estate specified in section 2 of the calculation, subject to property tax at the average annual value.

Section 3 calculations

Now on line 001 you need to indicate the code of the type of property. We talked about changes to this code in the commentary to section 2 of the calculation.

Line 030, filled in only if the property taxed at cadastral value is in common (shared or joint) ownership, indicates the organization's share in the right to the property.

And line 035 is filled in in relation to premises, the cadastral value of which has not been determined, and at the same time the building in which the premises is located is determined.

This line indicates the share of the cadastral value of the building in which the premises are located, corresponding to the share of the total area of the building.

In connection with the addition of the above lines, the previously existing lines 020 “Cadastral value as of January 1 of the tax period” and 030 “including non-taxable cadastral value” have been renumbered.

When filling out line 040 of section 3 of the calculation, you need to take into account innovations in tax benefit codes.

How to fill out the calculation

We will show you how to fill out a new form for calculating an advance payment of corporate property tax using a numerical example. In it we will fill out the calculation for the advance payment for the six months (Q2).

EXAMPLE 1. CALCULATION OF ADVANCE PAYMENT FOR PROPERTY TAX OF ORGANIZATIONS FOR HALF-YEAR

Example 1. Calculation of advance payment of corporate property tax for six months

LLC "Vector" is located in the city of Arkhangelsk, OKTMO code - 11 701 000.

The organization's balance sheet includes movable and immovable property - fixed assets recognized as objects of taxation, the residual value of which is:

as of 01/01/2017 – RUB 1,200,000;

- as of 02/01/2017 – RUB 2,300,000;

- as of 03/01/2017 – RUB 2,200,000;

- as of 04/01/2017 – RUB 2,800,000;

- as of 05/01/2017 – RUB 2,700,000;

- as of 06/01/2017 – RUB 2,600,000;

- as of July 1, 2017 – RUB 2,500,000.

Vector’s accountant reflected this data on lines 020 – 080 in column 3 of section 2 of the calculation.

The organization does not have benefits, so the accountant does not fill out column 4 of section 2 of the calculation.

The average value of property for the reporting period (line 120) is:

(RUB 1,200,000 + RUB 2,300,000 + RUB 2,200,000 + RUB 2,800,000 + RUB 2,700,000 + RUB 2,600,000 + RUB 2,500,000): 7 = RUB 2,328,571 .

The organization does not enjoy property tax benefits. Therefore, in all lines where data on benefits is reflected, the accountant added dashes.

The tax rate in force in Arkhangelsk is 2.2%. Her accountant entered line 170 of section 2 of the calculation.

The amount of the advance payment for the half-year (line 180) is equal to:

RUB 2,328,571 (line 120) × 2.2 (line 170) : 100: 4 = 12,807 rub.

The residual value of fixed assets related to movable property as of July 1, 2017 is RUB 1,200,000.

The residual value of the organization's immovable fixed assets as of July 1, 2017 was 1,300,000 rubles (2,500,000 rubles – 1,200,000 rubles). This amount is reflected in line 050 of section 2.1 of the calculation.

The organization owns an office building in Arkhangelsk, OKTMO code – 11,701,000. The building is included in the list of real estate objects for which the tax base is determined as their cadastral value. Its conditional cadastral number is 22:00:0000000:10011. The cadastral value of the building is 45,000,000 rubles. The organization also does not have benefits established by regional legislation.

The corporate property tax rate for an office building in 2017 is 2.2%.

The amount of the advance payment for the six months is 247,500 rubles. (RUB 45,000,000 × 2.2%: 4).

The company reflected these data in section 3 of the calculation.

The total amount of the advance payment for corporate property tax for the six months, reflected in section 1 of the calculation on line 030, is equal to 260,307 rubles. (12,807 + 247,500).

An example of filling out an advance payment calculation

What has changed in the declaration

The barcodes on all pages of the declaration have changed, and the field for indicating the TIN has been reduced from 12 to 10 characters. Fundamental innovations affected the title page, sections 2 and 3. In addition, a new section 2.1 “Information on real estate objects taxed at the average annual value” appeared.

Title page

It is no longer necessary to indicate the economic activity code according to the OKVED classifier on the title page.

Section 2

Unlike the previous declaration form, section 2 must be completed separately and also:

- along main gas pipelines, gas production facilities, helium production and storage facilities;

- for other objects necessary to ensure the functioning of real estate objects of main gas pipelines, gas production facilities, helium production and storage facilities.

For the listed objects, three conditions must be simultaneously met:

- objects were first put into operation during tax periods (calendar years) starting from 01/01/2015;

- objects are located wholly or partially within the borders of the Republic of Sakha (Yakutia), Irkutsk or Amur regions;

- During the entire calendar year, the facilities are owned by organizations that sell gas to Russian consumers.

In addition, the property type codes required to fill out line 001 of section 2 of the declaration have changed and become two-digit. In particular, separate codes are now installed:

- 07 – for property located in the internal sea waters of the Russian Federation, in the territorial sea of the Russian Federation, on the continental shelf of the Russian Federation, in the exclusive economic zone of the Russian Federation or in the Russian part (Russian sector) of the bottom of the Caspian Sea, used in carrying out activities for the development of offshore hydrocarbon deposits, including geological study, exploration, preparatory work;

- 08 – for the above-mentioned objects related to gas production;

- 09 – for public railway tracks and structures that are their integral technological part;

- 10 – for main pipelines, energy transmission lines, as well as structures that are an integral technological part of these facilities;

- 11 – for real estate objects included in the list of objects, the tax base for which is determined as the cadastral value;

- 12 – for real estate of a foreign organization, the tax base for which is determined as the cadastral value, with the exception of property with codes 11 and 13;

- 13 – for residential buildings and residential premises not reflected in accounting as fixed assets.

New tax benefit codes have been added that are required to fill out line 160 of section 2 of the declaration, namely:

- 2010257 - for movable property registered as fixed assets from 01/01/2013 (with the exception of railway rolling stock produced starting from 01/01/2013), registered as a result of the reorganization or liquidation of legal entities or the transfer (including acquisition) of property between interdependent persons;

- 2010258 - in relation to property recorded on the balance sheet of an organization - a participant in a free economic zone (FEZ), created or acquired for the purpose of conducting activities in the territory of a FEZ and located on the territory of this FEZ, for 10 years from the month following the month of registration of the specified property;

- 2010340 – in relation to property located in the internal sea waters of the Russian Federation, in the territorial sea of the Russian Federation, on the continental shelf of the Russian Federation, in the exclusive economic zone of the Russian Federation or in the Russian part (Russian sector) of the bottom of the Caspian Sea, used in the implementation of activities for the development of offshore hydrocarbon deposits , including geological study, exploration, and preparatory work.

A new line 215 has appeared to indicate the Kzd coefficient.

It is filled in if code 09 is indicated on line 001 of section 2 of the declaration - in relation to public railway tracks and structures that are their integral technological part, first registered as fixed assets, starting from 01/01/2017.

Section 2.1

This section will have to be completed by Russian and foreign organizations in relation to real estate specified in section 2 of the declaration, taxed at the average annual value.

Section 3

Now on line 001 you need to indicate the code of the type of property. We described changes to this code in the commentary to section 2 of the declaration.

table 2

Changes to filling out the lines of section 3 of the declaration

| Line code | It became | Was |

| 030 | To be completed only if the property, taxed at cadastral value, is in common (shared or joint) ownership. The organization's share in the right to the property should be indicated. | Filled out only by foreign organizations in the declaration for 2013. It was necessary to indicate the inventory value of the real estate property of a foreign organization as of 01/01/2013 |

| 035 | Filled out in relation to premises whose cadastral value has not been determined, and at the same time the cadastral value of the building in which the premises is located has been determined. You should indicate the share of the cadastral value of the building in which the premises are located, corresponding to the share of the area of the premises in the total area of the building | It was necessary to indicate the property tax-free inventory value of the real estate property of a foreign organization as of 01/01/2013 |

How to fill out a declaration

We will show you how to fill out a new tax return form for corporate property tax using a numerical example.

In it we will fill out a declaration based on the results of 2017. All numerical indicators are conditional.

EXAMPLE 2. REPORTING ON PROPERTY TAXES OF ORGANIZATIONS

Let’s continue the condition of example 1. Let’s assume that the residual value of fixed assets recognized as objects of taxation is:

as of 08/01/2017 – RUB 2,400,000;

- as of September 1, 2017 – RUB 2,300,000;

- as of October 1, 2017 – RUB 2,500,000;

- as of November 1, 2017 – RUB 2,400,000;

- as of December 1, 2017 – RUB 2,300,000;

- as of December 31, 2017 – RUB 2,200,000.

The data on the residual value for the period from 01/01/2017 to 12/31/2017 was reflected by the Vector accountant on lines 020 – 140 in column 3 of section 2 of the declaration.

The residual value of the organization's immovable fixed assets as of December 31, 2017 amounted to RUB 1,560,000. This amount is reflected in line 141 of section 2 of the declaration. The organization does not have benefits, so the accountant did not fill out column 4 of line 141.

The average annual value of property (line 150) is:

(RUB 1,200,000 + RUB 2,300,000 + RUB 2,200,000 + RUB 2,800,000 + RUB 2,700,000 + RUB 2,600,000 + RUB 2,500,000 + RUB 2,400,000 + 2 RUB 300,000 + RUB 2,500,000 + RUB 2,400,000 + RUB 2,300,000 + RUB 2,200,000) : 13 = RUB 2,338,462

The accountant calculated the tax base (line 190) as follows:

RUB 2,338,462 (line 150) – 0 rub. (line 170) = 2,338,462 rubles.

The tax amount for the tax period 2017 (line 220) is equal to:

RUB 2,338,462 (line 190) × 2.2 (line 210) : 100 = 51,446 rubles.

During 2017, advance tax payments were calculated:

For the first quarter of 2017 – 11,688 rubles;

- for the first half of 2017 – 12,807 rubles;

- for nine months of 2017 – 12,925 rubles.

The amount of advance payments was:

11,688 + 12,807 + 12,925 = 37,420 rubles.

The amount of tax on fixed assets to be paid additionally at the end of 2017 is 14,026 rubles. (51,446 – 37,420).

The residual value of fixed assets related to movable property as of December 31, 2017 is RUB 1,050,000. For an office building, taxed at cadastral value, for 2017 the organization paid advance payments in the amount of RUB 742,500. (RUB 45,000,000 × 2.2%: 4 × 3).

The amount of tax calculated for the year is 990,000 rubles. (RUB 45,000,000 × 2.2%).

The amount of tax for an office building to be paid additionally at the end of 2017 is RUB 247,500. (990,000 – 742,500).

The total amount of corporate property tax reflected in section 1 of the declaration is 261,526 rubles. (14,026 + 247,500).

Example of filling out a declaration

How to submit a calculation and declaration

Organizations that are not major taxpayers should report to the tax inspectorates (clause 1 of Article 386 of the Tax Code of the Russian Federation):

- at the location of the organization;

- at the location of each having a separate balance;

- at the location of each piece of real estate, in respect of which a separate procedure for the calculation and payment of tax has been established.

If a constituent entity of the Russian Federation has reporting periods for corporate property tax, then advance payments should be reported no later than 30 calendar days from the end of the corresponding reporting period (clause 2 of Article 379, clause 2 of Article 386 of the Tax Code of the Russian Federation):

- the first quarter, six months or nine months of the calendar year - when taxing property at the average annual value;

- the first quarter, second quarter and third quarter of the calendar year - when taxing property at cadastral value.

Moreover, if the last day of the period falls on a weekend or non-working holiday, the end of the period is postponed to the next working day (Clause 7, Article 6.1 of the Tax Code of the Russian Federation).

So, you need to submit the calculation:

- for the first quarter of 2017 - no later than 05/02/2017 (taking into account the postponement of the deadline that falls on a weekend);

- for half a year or for the second quarter of 2017 - no later than 07/31/2017 (taking into account the postponement of the deadline that falls on a weekend);

- for nine months or for the third quarter of 2017 - no later than October 30, 2017.

Please note: if the organization submitted the initial calculation of advance payments for the reporting periods of 2017 using a new form, then the updated calculations for these periods should also be submitted in the form approved by the commented order (letter of the Federal Tax Service of Russia dated April 14, 2017 No. BS-4-21/ 7145).

All organizations that have fixed assets recognized as objects of taxation must submit calculations of advance payments for property tax. The value of the residual value of such objects does not matter (clause 1 of Article 373, Article 374, clause 1 of Article 386 of the Tax Code of the Russian Federation).

What property is subject to tax? Russian And foreign organizations are defined differently. Read more aboutproperty tax in tax accounting in our article.

Who should not submit the calculation?

If an organization does not have fixed assets recognized as objects of taxation, it is not necessary to report property taxes. The grounds for this are clause 1 of Art. 373, art. 374, paragraph 1, art. 386 of the Tax Code of the Russian Federation, letter of the Ministry of Finance of Russia dated September 23, 2011 No. 03-05-05-01/74.

There is also no need to submit settlements in relation to preferential property related to oil production at offshore fields (paragraph 2, paragraph 1, article 386, paragraph 24, article 381 of the Tax Code of the Russian Federation). Include the remaining property that is subject to taxation in the calculation. Read more in the article,what property is taxable. Even if other benefits apply to this property. For example, movable property that belongs to 3–10 depreciation groups must be included in the calculation. Even if it was acquired after January 1, 2013 (letter of the Federal Tax Service of Russia dated December 17, 2014 No. BS-4-11/26159).

And of course, the calculation of advance payments for property tax (as well as the declaration for this tax) is not submitted by entrepreneurs and citizens. They do not pay such a tax in principle (clause 1 of Article 373 of the Tax Code of the Russian Federation).

Situation: who must submit calculations of advance payments for property tax - the founder of the trust management or the trustee?

Founder of trust management.

Taxpayers are required to submit tax calculations (subclause 4, clause 1, article 23, clause 1, article 386 of the Tax Code of the Russian Federation). And for objects transferred to trust management, the payer of the property tax is the founder of the trust management (Article 378 of the Tax Code of the Russian Federation). That is, an organization that transferred its property to a manager. Thus, it is she who must prepare and submit tax reports on property tax. A similar point of view is reflected in the letter of the Ministry of Finance of Russia dated September 23, 2008 No. 03-05-05-01/58, paragraphs 3–4 of paragraph 3 of the letter of the Ministry of Finance of Russia dated August 2, 2005 No. 07-05-06/216.

Situation: Is it necessary to submit calculations of advance payments for property tax if the residual value of fixed assets is zero? The organization applies a general taxation system.

Yes need.

Calculations of advance payments for property tax must be submitted by all payers of this tax (Article 386 of the Tax Code of the Russian Federation). And these are all organizations that have fixed assets that are taxed (clause 1 of Article 373, Article 374 of the Tax Code of the Russian Federation). The amount of the residual value of the property is not important - there is no such restriction in the Tax Code of the Russian Federation.

If the residual value of fixed assets recognized as an object of taxation is zero, the tax base and the amount of tax that must be indicated in the calculations will be equal to zero. However, the organization is required to submit estimates of advance property tax payments. This is confirmed by letter of the Federal Tax Service of Russia dated February 8, 2010 No. 3-3-05/128.

An organization may also have real estate objects, the tax base for which is their cadastral value. The amount of the advance payment for property tax on such objects does not depend on their residual value. This means that in this case the organization must also submit calculations of advance payments for property tax.

Calculation form

The form of calculation for advance payments of property tax has changed. Starting with reporting for the first half of 2017, calculations are provided in the form approved by Order of the Federal Tax Service of Russia dated March 31, 2017 No. ММВ-7-21/271@.

Let's figure out what you should pay attention to when calculating property taxes for organizations.

Due dates: tax and reporting period

The tax period is the calendar year (Clause 1, Article 379 of the Tax Code of the Russian Federation).

The reporting periods of the calendar year depend on the tax base (clause 2 of Article 379 of the Tax Code of the Russian Federation):

|

The tax base |

Reporting periods |

|

The tax is calculated based on the average annual value of the property |

I quarter, half year, 9 months |

|

The tax is calculated based on the cadastral value of the property |

I quarter, II quarter, III quarter |

Here are the dates for 2018:

for the first quarter – no later than May 4, 2018;

for the half year (2nd quarter) – no later than August 1, 2018;

for nine months (III quarter) – no later than October 31, 2018.

Attention: An organization may be fined for being late in calculating advance payments for property taxes.

Calculations of advance payments are recognized as documents necessary for tax control.

Firstly, sanctions for late submission of documents required for tax control are provided for in paragraph 1 of Article 126 of the Tax Code of the Russian Federation. The fine amount is 200 rubles. for each document not submitted.

Secondly, for untimely submission of such documents at the request of the tax inspectorate, the court may impose administrative liability on officials of the organization (for example, its head). The fine amount will be from 300 to 500 rubles. (Part 1 of Article 15.6 of the Code of Administrative Offenses of the Russian Federation).

It is worth noting that calculations of advance payments are not equivalent to tax returns (Clause 1, Article 80 of the Tax Code of the Russian Federation). Consequently, an organization cannot be fined for late submission of calculations under Article 119 of the Tax Code of the Russian Federation (letter of the Ministry of Finance of Russia dated May 5, 2009 No. 03-02-07/1-228, paragraph 15 of the information letter of the Presidium of the Supreme Arbitration Court of the Russian Federation dated March 17, 2003 No. 71, resolution of the Federal Antimonopoly Service of the East Siberian District dated January 18, 2006 No. A58-4095/2005-F02-6999/05-S1, Volga-Vyatka District dated April 27, 2006 No. A82-2065/2005-27, Far Eastern District dated May 31, 2006 No. F03-A51/06-2/1217, Moscow District dated September 16, 2008 No. KA-A40/8744-08).

Determination of the tax base

When determining the tax base, not all property is included in the tax base. We will divide property that is not involved in determining the tax base into two groups: exempt and preferential.

Tax exemption

The list of property that is not recognized as an object of taxation is given in paragraph 4 of Art. 374 Tax Code of the Russian Federation. For example, land plots and other environmental management facilities (water bodies and other natural resources) and others.

At the same time, fixed assets belonging to depreciation group I or II are excluded from the tax base, i.e., with a useful life from 1 year to 3 years inclusive (clause 8, clause 4, article 374 of the Tax Code of the Russian Federation).

Privileges

The benefits include property listed in Article 381 of the Tax Code of the Russian Federation. Let us dwell in detail on the benefit applied to movable objects registered as fixed assets from 01/01/2013 (clause 25).

If an organization applies this benefit, then it is necessary to follow regional legislation. Subjects of the Russian Federation are now solely vested with the right to establish benefits on their territory. If the region does not take advantage of this right, then from January 1, 2018, the benefits provided for in paragraphs 24 and 25 of Article 381 of the Tax Code of the Russian Federation will no longer apply on its territory.

Preparing for calculations

Let's distribute everything accounted for in accounts 01 and 03 of the Chart of Accounts into 5 groups:

|

№ |

Groups |

A comment |

|

Real estate for which the cadastral value has been determined |

The cadastral value of objects is posted on the official website of Rosreestr https://rosreestr.ru |

|

|

Real estate for which there is no cadastral valuation |

Real estate recorded on the balance sheet for which there is no cadastral value |

|

|

III |

Objects exempt from taxation |

The list is given in paragraph 4 of Art. 374 Tax Code of the Russian Federation |

|

Preferential objects |

The list is given in Art. 381 Tax Code of the Russian Federation |

|

|

Other |

Property that does not fall into any of the above groups |

Once we have decided on the fixed assets, we will move on to filling out the property tax calculation.

Where to submit the payment

To correctly determine where to submit the calculation of advance payments for property taxes, answer three questions:

- Is your organization the largest taxpayer?

- Based on what value was calculated the tax base for the property for which you are submitting calculations: from the average or cadastral?

- Does the organization have separate divisions with property on their balance sheet? And if so, how is the tax distributed among local budgets?

If your organization is the largest taxpayer, then for all objects, even those that are taxed at cadastral value, submit a single report at the place where the organization is registered as the largest taxpayer. This is stated in paragraph 1.5 of Appendix 6 to the order of the Federal Tax Service of Russia dated November 24, 2011 No. ММВ-7-11/895.

But if the organization is not one of the largest, then for each property with a cadastral tax base, submit separate calculations at the location of these objects. The Federal Tax Service of Russia sent such clarifications to the tax inspectorates by letter dated April 29, 2014 No. BS-4-11/8482.

Let's move on to the next question. Does the organization have separate divisions? If not, then submit the calculation for the property, the tax base for which you calculate from the average cost, to the inspectorate at the location of the organization.

For the property of separate divisions (the tax base for which is calculated from the average cost), report depending on the budget structure of a particular region. Property tax amounts or advance payments may:

- go entirely to the regional budget;

- partially or fully go to the budgets of municipalities;

- distributed among the settlements included in the municipality.

If in your region there is no distribution of property taxes between municipal budgets, then calculations of advance payments can be submitted centrally - at the location of the organization. But it's necessary . This is stated in paragraph 1.6 of Appendix 6 to the order of the Federal Tax Service of Russia dated November 24, 2011 No. ММВ-7-11/895.

Is property tax in the region credited (in whole or in part) to local budgets? There are several options, all of them are in the table below:

|

Where is the organization, its separate branches with a separate balance sheet or geographically distant real estate located? |

Which tax office should I submit reports to? |

How many reports to submit? |

How to reflect tax in reports |

|

In several municipalities under the jurisdiction of different tax inspectorates |

By location of each separate division with a separate balance sheet or geographically remote real estate |

For each division with a separate balance sheet and for each geographically remote property, submit separate calculations |

In the submitted forms, reflect only the tax, the payment of which is controlled by the tax office of the relevant municipality |

|

In several municipalities under the jurisdiction of one tax office |

By location of the organization's head office |

Submit a single report for all property on which you pay tax in the territory of the municipality |

Calculate the reporting tax separately for each municipality |

|

In one municipality |

In your reports, reflect all property taxes under one OKTMO code - the municipality at the location of the organization's head office |

Similar explanations are contained in paragraph 7 of the letter of the Ministry of Finance of Russia dated February 12, 2009 No. 03-05-04-01/08.

At the same time, the following is provided for municipalities such as districts. It will not be possible to provide a single calculation if, by decision of local legislators, part of the property tax is transferred to the budgets of the district’s settlements. Then you will have to submit separate calculations.

All these rules are spelled out in paragraphs 1 and 5 of Article 386 of the Tax Code of the Russian Federation, and are also set out in the letter of the Federal Tax Service of Russia dated April 29, 2014 No. BS-4-11/8482. The diagram below will help you avoid getting confused about where to pay property tax (including advances) and where to submit reports.table. .

Coordination of centralized reporting

Payments can be submitted centrally for all divisions of the organization only in agreement with your tax office. To do this, send a notification to the inspectorate at free form . In the document, indicate the structural units, their location and OKTMO codes, as well as the inspection to which the reports will be submitted.

This is stated in letters of the Federal Tax Service of Russia dated March 20, 2014 No. BS-4-11/5132 and dated December 23, 2013 No. BS-4-11/23185.

Situation: Is it possible to submit calculations of advance payments for property tax centrally - at the location of the head office of an organization, if in one subject of the Russian Federation it has several separate divisions with separate balance sheets?

The answer to this question depends on whether the property tax is distributed between local budgets or not (Clause 5, Article 56, Article 58 of the Budget Code of the Russian Federation).

If regional legislation does not provide for the transfer of part of the tax to local budgets, then in the reporting reflect the entire amount of property tax payable to the budget of the constituent entity of the Russian Federation. Including for separate divisions and real estate objects that are located on the territory of this subject of the Russian Federation. In this case, the organization has the right to submit tax reports centrally - at the location of the organization's head office. But first submitting reports centrally with your inspection.

For example, this procedure is established for organizations that have separate divisions or geographically distant real estate in Moscow. An organization that has separate divisions in different districts of Moscow with separate balance sheets on which property objects are listed can pay property tax and submit reports on such objects at the location of the head office (if located in Moscow) or one of such separate divisions. If an organization has geographically remote real estate properties in different districts of Moscow, then it can pay property tax and submit reports on such properties at the location of its head office in Moscow.

Similar explanations are contained in paragraphs 2–6 of the letter of the Ministry of Finance of Russia dated February 12, 2009 No. 03-05-04-01/08 and in the letter of the Federal Tax Service of Russia dated October 30, 2012 No. BS-4-11/18282.

It should be noted that for real estate objects, the tax base for which is determined as their cadastral value, calculations must be submitted only at their location. It does not matter how the tax is distributed in the region and whether the organization has the right to submit reports centrally. This conclusion can be drawn from letters of the Federal Tax Service of Russia dated June 2, 2014 No. BS-4-11/10451 and dated December 23, 2013 No. BS-4-11/23185.

If property tax amounts are credited (in whole or in part) to local budgets, then several options are possible. All of them are presented in .

At the same time, the following is provided for such municipal entities as municipal districts. An organization cannot submit a single calculation for property located on the territory of a municipal district if, by decision of the representative body of this municipal district, part of the property tax is credited to the budgets of its settlements.

This procedure is established by clause 1.6 of the Procedure for filling out the calculation of advance payments, approved by order of the Federal Tax Service of Russia dated November 24, 2011 No. ММВ-7-11/895.

An example of presenting calculations of advance payments for property taxes. Regional legislation does not provide for the transfer of part of the tax to local budgets

The head office of the organization, its separate divisions and geographically remote real estate objects are located on the territory of one constituent entity of the Russian Federation, but in different municipalities (the territory of each municipality is supervised by a separate tax office). Regional legislation does not provide for the transfer of part of the property tax to local budgets. The organization does not have real estate objects for which the tax base is their cadastral value.

The organization's accountant prepares one calculation of advance payments for property tax. In it, he indicates the total amount of the advance payment for all property that is located on the territory of a constituent entity of the Russian Federation (i.e., for the head office of the organization, its separate divisions and geographically remote real estate objects). The accountant submits this calculation to the tax office at the location of the organization's head office. Therefore, it indicates the OKTMO code of the municipality in which the head office of the organization is located.

An example of presenting calculations of advance payments for property taxes. Regional legislation provides for the transfer of part of the tax to local budgets. The territory of each municipality is supervised by a separate tax office

The head office of the organization, its separate divisions and geographically remote real estate objects are located on the territory of one constituent entity of the Russian Federation, but in different municipalities (the territory of each municipality is supervised by a separate tax office). Regional legislation provides for the transfer of part of the property tax to local budgets.

The organization's accountant prepares calculations of advance payments for property taxes for each municipality. Each calculation reflects the amount of the advance payment for the property located on the territory of the given municipality. The accountant submits the calculations to the tax authorities at the location of the organization’s head office, its separate divisions and geographically remote real estate. In each of the calculations, the OKTMO code for the corresponding municipality is indicated.

An example of presenting calculations of advance payments for property taxes. Regional legislation provides for the transfer of part of the tax to local budgets. The territories of all municipalities are supervised by one tax office

The head office of the organization, its separate divisions and geographically remote real estate objects are located on the territory of one subject of the Russian Federation, but in different municipalities (the territories of all municipalities are supervised by one tax inspectorate). Regional legislation provides for the transfer of part of the property tax to local budgets.

The organization's accountant prepares one calculation of advance payments for property tax. In it, he separately indicates the amount of the advance payment for each municipal entity, on the territory of which there are separate divisions and geographically remote real estate objects. For each amount, the OKTMO code of the corresponding municipality is indicated. The accountant submits this calculation to the tax office at the location of the organization's head office. largest taxpayers . They must submit tax reports electronically via telecommunications channels to interregional inspectorates for the largest taxpayers.

This is stated in paragraph 3 of Article 80 of the Tax Code of the Russian Federation.

Attention: If an organization is required to submit reports electronically, but submits them in paper form, it will be fined 200 rubles. for each calculation. This is stated in Article 119.1 of the Tax Code of the Russian Federation.

Calculation of property tax for legal entities

General filling requirements